Insurance: The Hidden Market Force Threatening Affordable Housing

Increasing insurance costs are making an already painful housing affordability crisis even worse. Our research shows how the current state of property and liability insurance—both of which multifamily housing providers must obtain—further strains the quantity and quality of affordable housing in the United States. Through research and interviews with nearly 40 affordable housing developers, providers, lenders, insurance industry participants, and tenant organizers, we map out the multiple intervention points at which property and liability insurance shape how affordable housing can be built and maintained.

We find that:

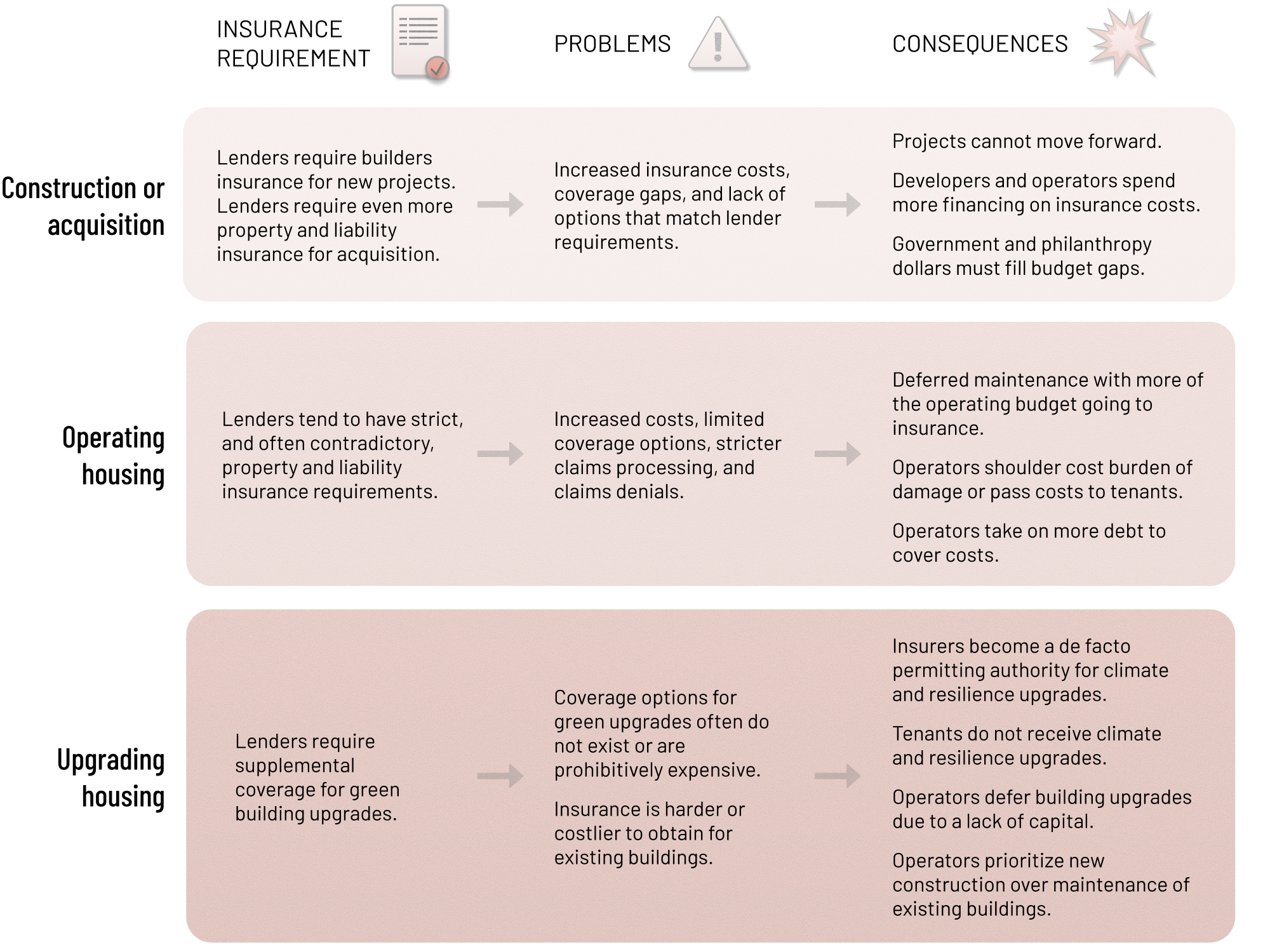

- The insurance crisis is hampering the development and viability of affordable housing supply. Faced with rising premium costs and even all-out denials of coverage, developers struggle to ensure adequate insurance coverage for new construction and acquisition/rehabilitation. Housing operators, for their part, shoulder more costs from damages, which they may pass on to tenants in the form of rent increases (where allowed), increased fees or deferred maintenance.

- Insurers have significant power over what gets built, serving as a de facto “permitting authority.” With their underwriting and claims payout decisions, insurers decide which existing buildings or locations are worthy of improvements, renovations, or retrofits.

- Housing operators are postponing building upgrades and green retrofits, often indefinitely, because of rising insurance costs. This impedes progress toward climate goals for the housing sector and can lead to deteriorating housing conditions for tenants.

Insurers shape affordable housing at every step.

To address the difficulties posed by insurance, affordable housing operators are increasingly turning to alternatives, like captive insurance programs. As the report documents, while these alternatives provide affordable housing operators with important release valves, the piecemeal nature of these tools inevitably falls short in tackling the magnitude of the crisis, especially when it comes to disaster coverage. Additionally, the public sector is often left picking up the tab, whether through additional subsidies to housing operators, tenants losing access to housing and turning to safety net programs, or post-disaster recovery aid. Meanwhile, insurance companies continue to prioritize profit-making rather than housing protection.

To address this crisis, CCI recommends large-scale interventions that put the public sector in the driver’s seat even before a crisis hits. Specifically, the report recommends:

- State or federal disaster insurance for all coupled with comprehensive risk reduction and adaptation, like the Housing Resilience Authority proposal.

- Creative municipal and state-level programs for pooling liability risk for affordable housing outside of profit-seeking entities, like those initiated by New York City Mayor Zohran Mamdani.

- Greater public investment and involvement in the affordable housing sector in a way that shifts away from housing as an asset to enshrining it as a social good, like CCI’s Green Social Housing proposal.